As life expectancies increase, you may need to plan for a longer retirement.

If you’re well prepared, this shouldn’t be a problem, and you’ll be able to enjoy a good quality of life throughout your retirement. However, if you don’t save enough, you may outlive your pension and have to adjust your lifestyle.

Fortunately, with our support, you may be able to prevent this.

Read on to learn more.

You may need to fund your retirement for 20 years or more

Figures from Statista show that the average life expectancy in the UK in 1970 was around 71.

At that time, the State Pension Age was 65 for men and 60 for women. Men with average life expectancies retiring at that age would have needed to fund their retirements for five years, while women would need savings to last 10 years.

In comparison, the Office for National Statistics (ONS) reports that the current average life expectancy of a 50-year-old is:

- 84 for men

- 87 for women.

This means that 50-year-old men retiring at their State Pension Age – which will be 67 – with an average life expectancy would need to fund their retirement for 18 years. Meanwhile, women would need to cover living expenses for 20 years.

What’s more, you might live for longer than average and you may want to retire before reaching State Pension Age.

Consequently, you could need to fund your lifestyle for more than 20 years, increasing your chances of running out of savings in retirement.

Drawing sustainably from your pension helps you maintain your pot throughout retirement

When you retire and begin drawing from your pension, it’s important to consider how much you take each year, as well as the growth of your remaining savings.

If your withdrawal rate far exceeds the investment growth on the savings left in your pension, you could quickly deplete your pot and risk running out of money in retirement.

Conversely, if you balance the withdrawal rate with investment growth, you can draw sustainably from your pension, so your savings are more likely to last throughout retirement.

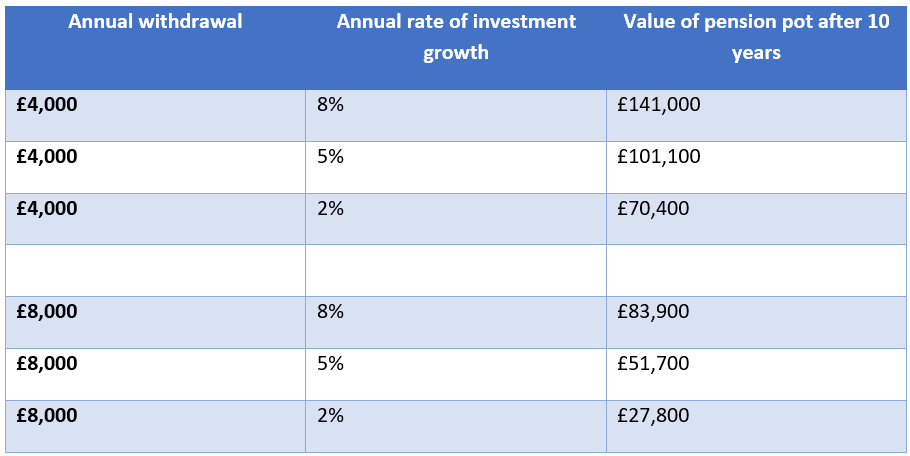

Figures from the Actuarial Post demonstrate how this works.

The following table compares the effects of various withdrawal rates and investment growth levels on a £100,000 pension pot after 10 years.

Source: The Actuarial Post

As you can see from these figures, a lower withdrawal rate of £4,000 combined with a moderate level of growth at 5% would sustain the value of your pot after 10 years. This is despite the fact you’re drawing a regular income from the pension.

However, if you were to make larger withdrawals of £8,000, the total value of your pot would fall, even if you achieved relatively high growth of 8%.

If you saw average growth of 5%, the value of your pot would be almost halved in a decade. You could spend your entire pension in around 20 years if you continued depleting your pot at this rate.

These figures are illustrative. If you have a larger retirement fund, you can draw a higher income. However, the same concept applies – it’s important to generate income sustainably without depleting your pension pot too quickly.

There are several ways you could increase your chances of achieving this.

3 ways to make sure you don’t outlive your pension savings

1. Consider increasing your pension contributions

The more you have in your pension, the longer it can support you in retirement. So, if you’re concerned about running out of money in retirement, you may want to consider increasing your pension contributions now to build your pot faster.

Even a small increase could make a significant difference in the long term as you benefit from investment growth and compound returns on your pension savings.

We can review your contributions with you to decide what you can comfortably afford to pay in, helping you secure your retirement without making sacrifices to your current lifestyle.

2. Create a retirement budget

As the figures above demonstrate, a higher withdrawal rate could deplete your savings quickly, even if you see significant investment growth. That’s why it’s important to take only what you need from your pensions each year.

Creating a retirement budget that lists all your expenses allows you to see precisely what level of income you need to draw each year. This prevents you from unnecessarily taking too much from your pension, meaning you can leave as much invested as possible.

You can also use your budget to see whether there are areas where you might cut back on spending and make your retirement savings go further.

3. Manage your investments carefully throughout retirement

If you generate a healthy level of investment growth on your pension, you may be able to sustain or even increase the size of your pot, while also drawing an income from it. This means you can continue funding your lifestyle throughout retirement without worrying about running out of money.

That’s why it’s vital to manage your investments carefully in retirement to ensure you achieve adequate returns.

We can support you with this by reviewing your investments regularly and making adjustments as needed to help you grow your pension savings.

Get in touch

With our support, you can reduce the chances of outliving your pension savings.

Please give us a call on 01276 855717 or email info@braywealth.com today to learn more.

Please note

This article is for general information only and does not constitute advice. The information is aimed at retail clients only.

All information is correct at the time of writing and is subject to change in the future.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates, and tax legislation may change in subsequent Finance Acts.

Your pension income could also be affected by the interest rates at the time you take your benefits. The tax implications of pension withdrawals will be based on your individual circumstances, tax legislation, and regulation, which are subject to change in the future.

The value of investments and any income from them can fall as well as rise and you may not get back the original amount invested.

Approved by the Openwork Partnership on 30/09/2025

Production

Production